2024 Sea Change in LNG Routes

SynMax Storytelling

The Global LNG Routes Reconfiguration Continues Amid Wars, Drought, and New Trade Economics

Leslie Palti-Guzman & Vivek Patil | 16 January 2025

The Decline of Two Vital Shipping Links

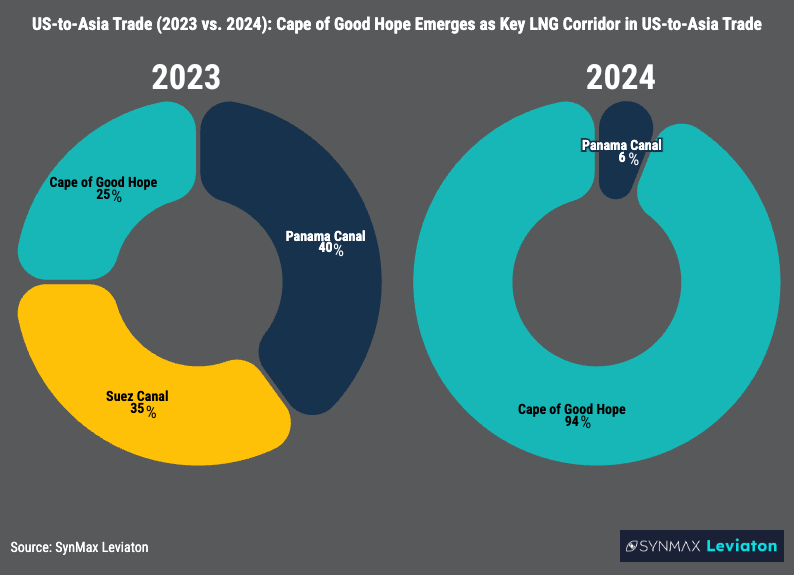

For much of global commerce, two key passageways — the Panama and Suez Canals – have long interconnected the Americas and Europe with Asia, optimizing time, freight costs and efficiency. However, LNG players have largely avoided both of these trade routes this past year, favoring instead the longer detour around the Cape of Good Hope.

This shift toward the Cape of Good Hope has been driven primarily by security risks from Iran-backed Houthi attacks in the Red Sea, compounded by severe bottlenecks at the Panama Canal caused by prolonged drought conditions.

Challenges Started to Emerge in 2023

The Panama Canal bottlenecks, driven by severe drought, have disrupted all shipping industry segments since early 2023. Gatún Lake, the Canal’s primary reservoir, reached historically low water levels. As a result, the Panama Canal Authority implemented conservation measures, transit restrictions and logistical adjustments to sustain operations

Despite these challenges, the impact on LNG trade in 2023 was largely downplayed by traders. The Panama Canal continued to serve as a critical connector between the Atlantic and the Pacific basins, remaining the most utilized route for shipping LNG to JKTC (Japan, Korea, Taiwan, China). The number of US LNG cargoes shipped to Asia using the Panama Canal in q3 2023 was still 38, compared to only 10 vessels a year after over the same period.

Meanwhile, the Suez Canal had not experienced any disruptions since the Ever Given blocked the Suez Canal in 2021. However, in late 2023, the Yemen-based Iran-backed Houthi group started targeting vessels in the Red Sea, with a notable escalation in attacks reported in December 2023. As a result, major shipping companies have adjusted their operations to bypass Bab al-Mandab Strait and the Canal. Since mid-January 2024, the Red Sea route has remained off-limits to Western LNG players, which have used alternative routes instead.

The 2024 Avoidance of Two Major Routes Redefines Trade Flows

The dual avoidance of the Panama and Suez Canals for LNG transit became the new normal in 2024, facilitated by weak freight rates.The stability of spot LNG shipping costs, despite the longer detours around the Cape of Good Hope, can be attributed to the influx of new LNG tankers entering the market at a time of only modest supply increases. Suppliers have largely absorbed the costs of these extended voyages, including those caused by increased boil-off losses.

Despite a modest improvement in water levels during the rainy season in Spring, the LNG industry continued to avoid the Panama Canal. Instead, it prioritized delivery and cost predictability via the Cape of Good Hope. In 2024, 94% of US LNG destined for Asia used the Cape of Good Hope route, adding approximately 20 days of transit time compared to the Panama Canal, and 10 days compared to the Suez Canal, according to SynMax Leviaton.

As a result, the US-Europe corridor strengthened in 2024, with 52% of US LNG exports heading to Europe. Meanwhile, Qatar bolstered its trade relations with Asia, with 80% of Qatar’s LNG exports landing in Asia (up from 75% in 2023). Within this share, 24% of volumes flowed to China and 14% to India. Meanwhile, Russia tried to maximize the utilization of the Northern Sea Route, but Western sanctions successfully curtailed imports from the new Arctic-2 LNG project. Name-and-shame pressures targeting buyers of Russian spot LNG have started to deter trade.

A Telling Comparison Route by Route

2024 Was a Worse Repeat of 2023 for the Panama Canal, Marked By Drought and Pricey auctions

The Canal faced its driest conditions in history in 2024, with no easy fix in sight. Alleviating the crisis will require a costly, multi-year plan, with the responsibility falling on both the government, and the Panama Canal Authority (PCA). However, the Panama government has deferred key investments and critical water project decisions since 2018, exacerbating the issue.

Most transit restrictions from 2023 continued in 2024. The (PCA) managed to increase daily transit on all segments to an average of 27 vessels, yet this remained far below the historical average of 36. The Panama Canal has never prioritized the LNG tanker segment, as the container segment represents a larger and more predictable chunk of its revenues.

In addition, high auction fees further disincentivized the PCA from addressing congestion. Despite a 20% decline in transits between 2023 and 2024, the Canal’s revenue increased by $30 million year-over-year, reaching $3.38 billion in 2024. This increase was largely due to auctions that raised slot values from $83,000 to as high as $4 million. As long as companies were willing to pay, the bottlenecks would have persisted. However, incoming President Trump’s threats to pressure Panama into addressing the Canal’s reliability will likely mark a turning point.

In 2024, 94% of US LNG bound for Asia took the Cape of Good Hope route. This longer route increased monetary and environmental costs. Asian buyers, who initially invested in US LNG with the expectation of shorter transit times through the Canal, now face increased delay and fleet utilization. If the Canal’s reliability continues to deteriorate, these buyers will invest further in other jurisdictions such as Mexico and Canada, for their long-term energy needs.

Believing that LNG Trade Is Better Off Without the Red Sea Route Is a Myth

Since mid-January 2024, no LNG tankers, except for two Russian-affiliated vessels, have used the Red Sea route due to heightened security risks. In 2024 alone, the Houthis targeted more than 89 vessels, creating an untenable environment for LNG trade through this critical corridor.

Despite these challenges, the LNG market has adapted by utilizing alternative routes, with shipping rates remaining weak. In the second half of 2024, rates had fallen to roughly $20,000-30,000 per day in the spot market, softening the financial blow of longer routes.

However, the notion that the LNG market is better off without the Red Sea route is a myth. The industry has much to gain from reconnecting the Pacific and Atlantic basins via the Suez Canal. Shorter routes means less methane and CO2 emissions, as well as lower shipping costs resulting in improved competitiveness for commodity trading.

The Cape of Good Hope Route is the New Favorite

The use of the Cape of Good Hope for US LNG shipments to Asia has surged fivefold this year compared to 2023 according to SynMax Leviaton data, as traders increasingly bypass both the Red Sea and the Panama Canal. The Cape of Good Hope has emerged as the preferred route for US LNG exports to Asia at a time when US exports to Asia increased by 22% compared to last year, reaching ~29 mt in 2024.

Currently, 81% of US LNG cargoes to Japan transit via the Cape of Good Hope. This marks a dramatic shift from 2023 when Japan relied on the Cape of Good Hope for only 13%, while the Panama Canal accounted for 66% of its LNG imports, and the Suez Canal for 21%.

The US Will Weight In on the Reopening of These Strategic Routes

The restoration of the Red Sea shipping route remains a long-shot, but the recent shift in Western strategy towards an offensive approach against the Iran-backed Houthi threat is likely to continue under the new US administration. LNG traders will closely monitor the evolving situation in 2025 to assess the security of this critical passage.

Meanwhile, President Trump's “maximum pressure” campaign on Panama aims to accelerate progress on the delayed Rio Indio water project. The Canal will likely announce public tenders in 2025 for the $1 billion initiative. However, a return to “business as usual” transit through the Panama Canal is unlikely before 2027 at the earliest.

The Future of US LNG Routes Will Hinge on Trade Evolution and Geopolitics

The future of US LNG trade routes will not only depend on the restoration of the Suez and Panama Canals as safe and reliable passages, but also on evolving trade relations. While Europe continues to dominate as the largest consumer of US LNG, relying on it for energy security, Asia is expected to drive global demand growth in the coming years, shaping the direction of shipments.

The growing politicization of US LNG will also play a critical role in determining destinations. While US-China trade relations may be caught in the crossfire of potential trade wars, other countries could leverage increased US LNG imports to strengthen bilateral ties with the new administration.